FW-R-4 + 5: Utilisation of raw timber and timber construction quota

2023 Monitoring Report on the German Strategy for Adaptation to Climate Change

2023 Monitoring Report on the German Strategy for Adaptation to Climate Change

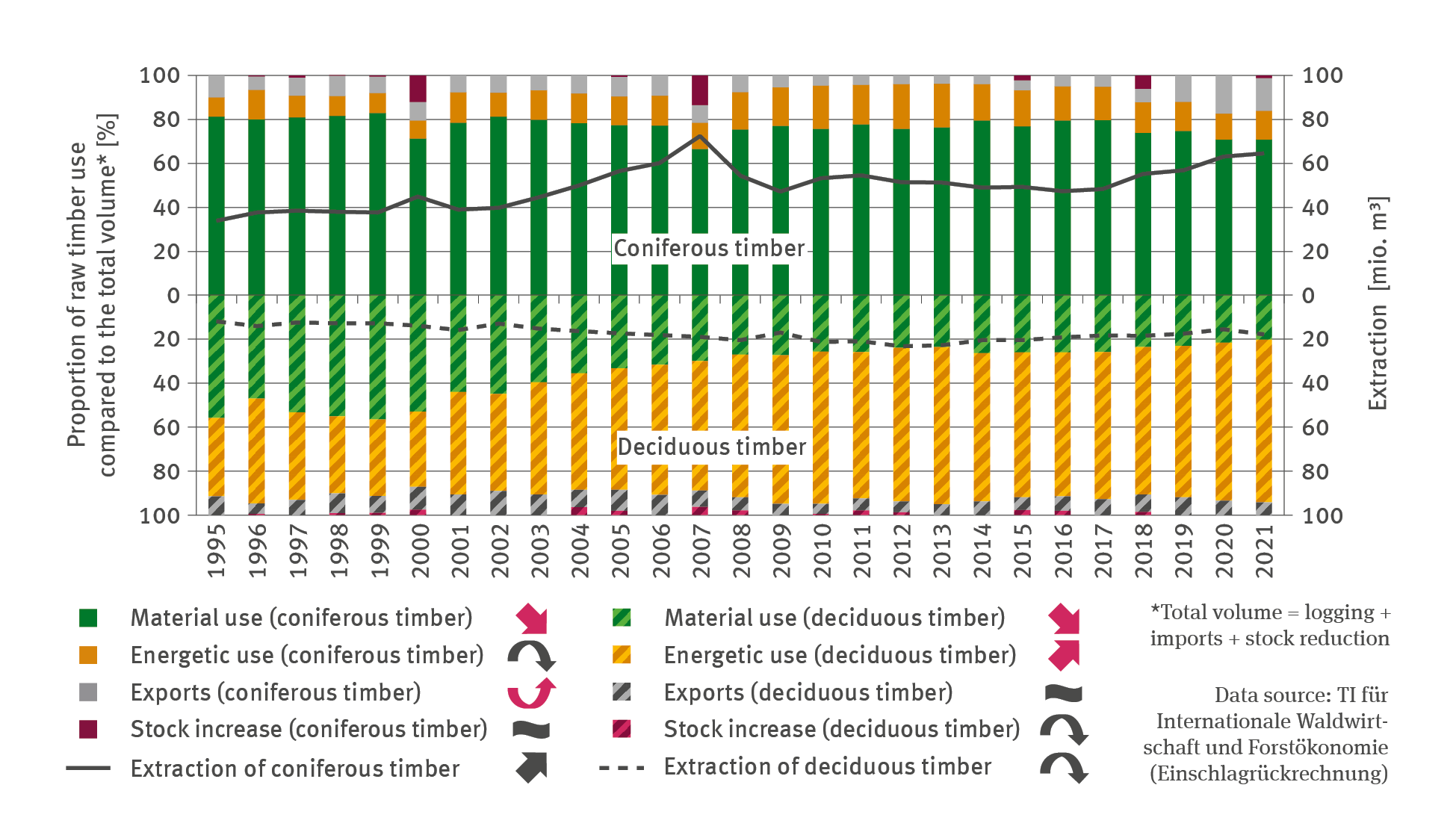

Forest transformation and the large amounts of calamity timber, especially in recent years, pose new challenges for the timber market. For climate protection reasons, it is important to find ways for the material utilisation of timber wherever possible, and preferably domestically. Given that deciduous timber is still clearly used predominantly for energy generation, the challenge is to open up new potentials for the use of this type of timber in producing material objects.

The building sector plays a major role in the material utilisation of timber. Especially in the residential building sector, the use of wood is increasing. However, there are many other potentials remaining to be opened up, especially in respect of non-residential buildings. Owing to its more favourable properties, it is predominantly coniferous timber that is used in the building sector. By contrast, the use of deciduous wood in the building sector is still in its infancy.

Both the forest transformation in favour of more vigorous and climate-resilient forests and the calamities of recent years (cf. Indicator FW-I-5) have made substantial impacts on the timber market. Overall, timber extraction from German forests has increased since 1994, latterly especially in respect of coniferous timber. This demonstrates the extensive efforts to bring timber from site-inappropriate coniferous stands and from calamity areas into ‘controlled use’. This can be done only as long as the capacities in the wood-processing industry are not overstretched by the amounts of raw timber to be processed. Such capacity overloads are reflected in mounting stock levels and / or exports, and they usually lead to the collapse of prices paid for raw timber. The distinctly higher exports of coniferous timber from 2019 to 2021 indicate that Germany’s wood-processing industry was unable to cope with the high volumes of calamity timber on offer. Against this background, the question arose to what extent it might be possible to treat calamity areas increasingly as a source of passive deadwood enrichment; in other words to waive its removal, insofar as there is no risk of direct hazards arising in terms of forest and health protection or in terms of road safety.

Forest transformation aims at a more mixed composition of stands where in particular site-adapted deciduous tree species play an important role. This would mean for the future timber market – albeit with some considerable delay – that a higher yield of deciduous timber could be expected. It would be essential to increase sales opportunities for this deciduous timber, above all and as far as possible in the domestic market. To this end, new utilisation potentials for deciduous timber would have to be opened up or developed; it would therefore be necessary to expedite research; and timber processing in sawmills would have to be developed to a higher level. As far as climate protection is concerned, the utilisation of deciduous timber will have to be more focused on its use for making material objects, in order to maintain the timber’s long-term function as a carbon sink. Currently, however, 70 % of deciduous timber is used as a source of energy. By now, firewood, woodchips and pellets for the generation of heat and power have become mass products. The intention is to replace fossil fuels and to reduce greenhouse gas emissions. However, this means that the CO2 previously stored in wood is released to the atmosphere. For long-term carbon sequestration it is therefore preferable to use deciduous timber for the production of material products that have some longevity. In sum, there are close connections between climate protection, climate adaptation and opening up further potentials in the timber market. The increased use of deciduous timber for the production of material objects continues to present challenges. Construction products made of deciduous timber are being developed, but so far official approval granted for such products has been limited. Overall it is true to say that the market for construction material made from deciduous timber is still in its infancy. As far as the wider use of deciduous wood is concerned, there is a need of further research and development, and it will also be necessary to gain more experience in this field. Also with regard to interior fittings, the situation is challenging, as currently trends lean towards perfect wood-imitation flooring and voluminous but lightweight furniture.

Overall, the timber construction quota is on the increase. However, statistics on building products so far do not differentiate between the proportions of deciduous versus coniferous timber. In 2021, a fifth of all residential buildings, measured by the number of building permits, were predominantly made of timber. In this context, the focus is on the field of one- and two-family houses. As far as multi-family houses are concerned, the use of timber is also on the increase, but this is still limited to a distinctly lower level. With regard to non-residential buildings, the timber construction quota is strongly characterised by extensions to individual buildings (complexes). For example, the completion of two large-scale projects (holiday resort) in 2018, comprising a total of 680 buildings in timber construction increased the timber construction quota to over 20 %120.

In order to achieve a trend reversal towards more material utilisation of deciduous wood, it will be essential to open up additional potentials for material utilisation – way beyond the building sector – in line with the objectives of the National Bioeconomy Strategy121. For example, one relevant substitution potential is envisaged for using deciduous timber in lieu of synthetics based on mineral oil or in lieu of metals, thus achieving a trend reversal towards biogeneous raw materials. The range of potential applications also includes clothing and textiles for home furnishings made of timber-based cellulosic fibres. Such potentials are of increasing interest, given that climate change has made the cultivation of cotton more difficult, thus basically making wood fibre production more competitive.

120 - FNR – Fachagentur Nachwachsende Rohstoffe e.V. 2019: Charta für Holz 2.0 – Kennzahlenbericht 2019 Forst & Holz, 48 pp. https://www.fnr.de/fileadmin/charta-fuer-holz/dateien/service/mediathek/WEB_BMEL_Kennzahlenbrosch%C3%BCre_WPR_091019.pdf

121 - BMBF – Bundesministerium für Bildung und Forschung & BMEL – Bundesministerium für Ernährung und Landwirtschaft (Hg.) 2020: Nationale Bioökonomiestrategie. Berlin, 64. pp. https://www.bmel.de/SharedDocs/Downloads/DE/_Landwirtschaft/Nachwachsende-Rohstoffe/nationale-biooekonomiestrategie-langfassung.html.

The UBA’s motto, For our environment (“Für Mensch und Umwelt”), sums up our mission pretty well, we feel. In this video we give an insight into our work.

Due to the large number of enquiries, there may be delays in responding. We ask for your understanding.