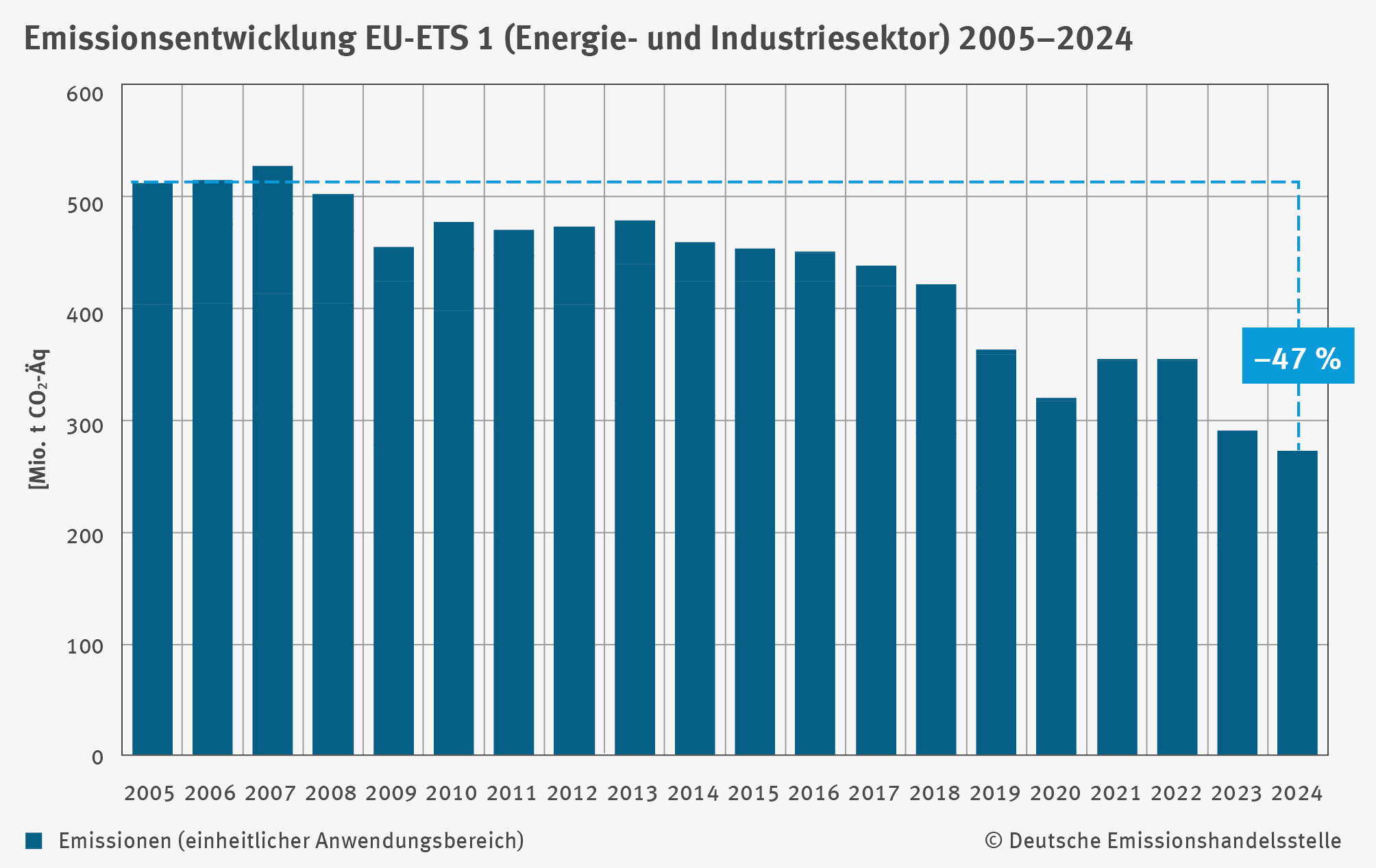

German emissions nearly halved in 20 years of trading

A significant reduction in climate-damaging emissions can be observed in the European Emissions Trading Scheme (EU-ETS 1). Since the launch of emissions trading 20 years ago, German installations under the EU-ETS 1 have reduced their emissions by around 47 percent. Across Europe, emissions under the EU-ETS 1 have fallen even more sharply by 51 percent. This means that since 2005, emissions have roughly halved, according to the German Emissions Trading Authority (DEHSt) at the German Environment Agency (UBA). Last year, emissions from installations subject to emissions trading in Germany fell by 5.5 percent. The EU-ETS 1 covers climate-damaging emissions from energy-intensive industries, the energy sector, intra-European aviation, and, since 2024, also maritime transport.

Dirk Messner, President of the UBA: “Since its introduction, emissions trading has developed step by step into the central climate protection instrument in Germany and Europe. Together with the national emissions trading scheme, the two systems currently cover around 85 percent of Germany’s greenhouse gas emissions. Revenues of approximately 18.5 billion euros last year form the key pillar of financing for the Climate and Transformation Fund of the Federal Government.”

Daniel Klingenfeld, Acting Head of the 'Climate Protection, Energy, German Emissions Trading Authority' Division at the UBA : “In the upcoming negotiations on the realignment of European climate policy for the period from 2030 onwards, we are using our expertise to support the consistent further development of emissions trading: Embedded in an effective mix of instruments, emissions trading will make a decisive contribution to achieving the statutory climate targets of Germany and the EU. The UBA’s projections for future national emissions trends from March this year have clearly highlighted the significant need for action. This applies especially to the transport and buildings sectors, where, from 2027 onwards, European emissions trading for fuels – the so-called EU-ETS 2 – will take effect.”

In 2024, the 1,716 stationary installations in Germany covered by the EU-ETS 1 emitted around 273 million tonnes of carbon dioxide equivalents (CO2-eq). This corresponds to a reduction of about 5.5 percent compared to the previous year.

Energy: In 2024, the decline in emissions from energy supply continued: They fell by 9.5 percent in 2024 compared to the previous year, reaching 171 million tonnes of CO2 equivalents. The main reasons for this are the growing share of renewable energies, the declining electricity generation from hard coal and lignite power plants, and the increase in the negative electricity trade balance with other countries (net imports). Compared to 2005, emissions from German energy installations covered by the EU ETS 1 have fallen by about 54 percent. Thus, the overall decline in emissions from German installations in the EU ETS 1 is driven by the energy sector.

Industry: In 2024, emissions from energy-intensive industries in Germany amounted to 102 million tonnes of CO2 equivalents – almost the same as the previous year, with a slight increase of 1.1 percent. Production development plays a central role in this context. All industrial sectors saw an increase in emissions, with the exception of cement clinker (-10 percent). Here, the decline in cement clinker production amounted to almost 9 percent. The most significant increases in emissions were observed in installations for the production of non-ferrous metals (+15 percent) and in the chemical industry (+9 percent). Compared to 2005, emissions from German industrial installations in the EU ETS 1 is around 29 per cent.

Aviation: Air traffic has continued to rise significantly, reaching the pre-pandemic level of 2019. In total, 75 aircraft operators in Germany were subject to emissions trading obligations in 2024, with aggregated emissions of around 8.9 million tonnes of CO2 equivalents. The increase in emissions compared to the previous year was around 16 percent. The growth trend that began in 2022 is therefore continuing. Aviation has been included in the EU ETS 1 since 2012. Currently, there is a general reporting and submission obligation only for emissions from flights that depart and land within the European Economic Area (EEA).

Maritime transport: Since 2024, CO2 emissions from ships with a gross tonnage (GT) of at least 5,000 have been subject to reporting and submission obligations under the EU ETS 1. This includes 100 percent of emissions in the ports of a Member State as well as 100 percent of emissions from voyages between ports within the EEA. For emissions on routes between EEA ports and ports outside the EEA, a levy of 50 percent applies. A reliable evaluation of shipping emissions for the year 2024 will only be possible in the follow-up report, as by the editorial deadline of this report, a significant share of emissions reports was still outstanding.

Germany and Europe: Emissions from all installations participating in the EU-ETS 1 (in the 27 EU Member States as well as Iceland, Liechtenstein, and Norway) also decreased in 2024: According to the data from the European Environment Agency (EEA) , emissions in 2024 declined by 6.5 percent compared to the previous year, to around 1.03 billion tonnes of CO2-eq.

Emissions trading and total emissions: According to the UBA estimate from March 2025, total emissions from all sectors in Germany are expected to decrease by 3.4 percent in 2024. The reduction in the EU‑ETS 1 thus exceeded the development of total emissions by a significant margin. The share of the EU-ETS 1 in Germany's total emissions is approximately 43 percent.

Further information:

German Emissions Trading Authority (DEHSt): The DEHSt at the German Environment Agency is responsible for implementing the EU-ETS 1, the national emissions trading for fuels (nEHS), as well as the European emissions trading for fuels (EU-ETS 2). It is also responsible for the administration of project-based mechanisms and the payment of subsidies to electricity-intensive companies to compensate for indirect CO2 costs (electricity price compensation). Since the end of 2023, the DEHSt has also served as the national authority responsible for the new CO2 border adjustment system ( CBAM ).

Associated content